Despite an initial pullback in the recovery timeline caused by a surge in infections from a new Omicron variant of the COVID-19 virus in December and January, continued improvement in top-line metrics for U.S. hotels is expected for the remainder of this year and next, according to PwC’s U.S. Hospitality Directions: May 2022 report.

While leisure travel continued to drive much of lodging’s demand in Q1, individual business travel and group business has started to emerge as we head into the warmer months. Strong leisure business is expected to cause demand compression over the summer, driving room rates and resultant RevPAR levels to new highs. If tensions ease in Ukraine, and immunity levels continue to increase domestically, a stronger Q4 driven by a resurgence in business transient and group demand is expected.

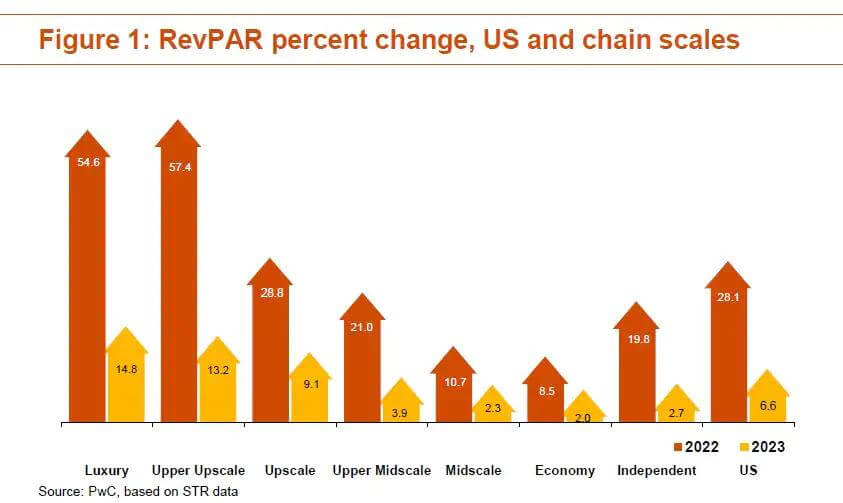

PwC expects annual occupancy for U.S. hotels this year to improve slightly from its November 2021 outlook, increasing to 63.1%. As in the last outlook, the big story remains room rates. ADR surpassed comparable 2019 levels in every month of Q3 and Q4 last year, and in February, March and April this year (January missed by $0.28). RevPAR in March and April exceeded comparable 2019 levels, and this is expected to continue through the forecast period. PwC now expects ADR to increase 16.9% for the year, with resultant RevPAR up 28.1%—approximately 106% of pre-pandemic levels, on a nominal dollar basis.

“Despite volatility in the financial markets and heightened concerns over the humanitarian crisis in Ukraine, we now expect U.S. hotels to surpass 2019 RevPAR levels this year, driven by strong growth in room rates stemming from focused revenue management strategies of operators,” said Warren Marr, managing director, U.S. Hospitality & Leisure

Trends and highlights

- With slowing vaccinations rates (66% of the U.S. population was fully vaccinated as of May 17, according to the Mayo Clinic) and new variants continuing to infect, coupled with volatility in the financial markets and geopolitical stress resulting from Russia’s invasion of Ukraine, lodging’s recovery could still be bumpy this year.

- In 2023, PwC expects demand growth from individual business travelers and groups to more than offset a potential softening in leisure demand (as international leisure travel continues to recover and people who took vacations domestically over the past two years, venture abroad). Growth in both occupancy and ADR is expected, with a year-over-year rebound in RevPAR of 6.6%—approximately 114% of pre-pandemic levels.

- Challenges to this outlook include the ongoing conflict in Ukraine, the potential impact of the Fed’s increases in interest rates on the U.S. economy, and any new variants of the virus.