After a two-year contraction that kept investors largely on the sidelines, U.S. hotel sales transactions rebounded in 2025—and the ripple effects are being felt far beyond the deal table. A surge in ownership changes is triggering an equally significant wave of property renovations and brand conversions.

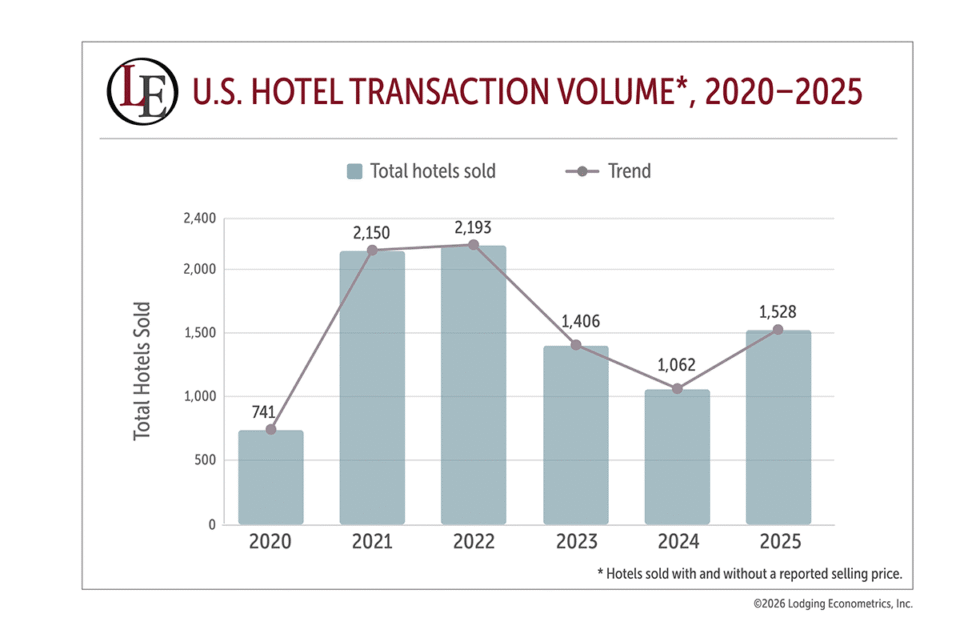

According to Lodging Econometrics (LE), total U.S. hotel transactions reached 1,528 hotels and 186,925 rooms in 2025, a 44% increase in hotels sold and a 49% jump in rooms transacted compared to 2024’s 1,062 hotels and 125,176 rooms. The recovery stands in even sharper contrast against 2023’s 1,406 transactions—a substantial step down from the 2,193 hotels that traded during the 2022 peak. By any measure, 2025 marked a clear inflection point.

The slump and what drove it

The 2023–2024 pullback reflected several converging pressures. The Federal Reserve’s interest rate hikes made hotel financing significantly more expensive, and sellers and buyers couldn’t agree on price—sellers still expected pre-rate-hike values while buyers needed steeper discounts to make the numbers work. At the same time, the post-pandemic travel boom was cooling, with urban and corporate hotel demand slower to recover than leisure, making future revenue harder to predict. Escalating insurance costs—particularly in coastal and sun-belt markets—added yet another layer of expense that buyers had to account for, which meant lower offers.

What changed in 2025

The Fed’s pivot to rate cuts beginning in late 2024 was the clearest catalyst. As financing conditions eased, previously stalled deals began moving again. Buyers re-engaged, lenders extended hospitality credit with greater flexibility and RevPAR stability across most chain scales gave underwriters confidence in forward cash flows. By Q4 2025, LE recorded 581 hotels and 74,134 rooms transacting in a single quarter—the strongest showing since 2022.

What makes this transaction cycle especially significant is what happens after closing. LE’s tracking of hotel sales from the past 12 months reveals 237 properties already undergoing or planning significant renovations and/or brand repositionings as a direct result of a change in ownership—and that represents a substantial, well-funded pipeline of opportunity for vendors and suppliers. New owners typically arrive with capital for improvement, whether that means a full property renovation, a brand change that triggers brand-standard upgrades or targeted reinvestments. For suppliers, manufacturers and service providers operating in the hospitality vertical, these 237 properties—and the many more not involved in transactions—aren’t just renovation projects. They’re active buying decisions, backed by owners with the motivation and budget to move quickly.

Notable deals illustrating the trend

Several transactions capture both the scale of activity and the renovation-and-conversion dynamic driving it. In New York, the InterContinental Times Square (607 rooms) sold for $230 million and will see renovations to guestrooms, public spaces and dining venues; the Dominick Hotel (391 rooms) traded for $175 million with a planned conversion; and NoMo SoHo (263 rooms) sold for $125 million with renovations slated. The Westin Cincinnati (456 rooms) sold for $62 million with a full-scale renovation planned later this year. The nearby 21C Museum Hotel Cincinnati (156 rooms) changed hands for $25 million and will undergo a $19.8 million renovation-conversion.

Looking ahead

As interest rates continue their gradual descent and buyer confidence deepens, LE projects sustained deal volume through 2026—and with it, continued renovation and conversion activity.

For more information on renovation, conversion and sales transaction activity in the United States with specific project details and decision-maker contact information, please contact Lodging Econometrics 603-431-8740, ext 0025 or [email protected].