The U.S. hotel industry maintains a steady development pipeline, though current activity reflects a more cautious approach amid near-term challenges. The current selective development environment suggests industry participants are making strategic decisions based on fundamental demand drivers, which will position new projects for success.

According to Lodging Econometrics’ (LE) Q1 2025 U.S. Hotel Construction Pipeline Trend Report, the total pipeline has expanded to 6,376 projects encompassing 749,561 rooms—representing a 5% increase in projects and 7% growth in rooms compared to Q1 2024. Most significantly, the 10% increase in projects and 13% rise in rooms in the early planning stage signals developer confidence in the long-term prospects of the hospitality sector, suggesting that industry stakeholders remain optimistic about future demand.

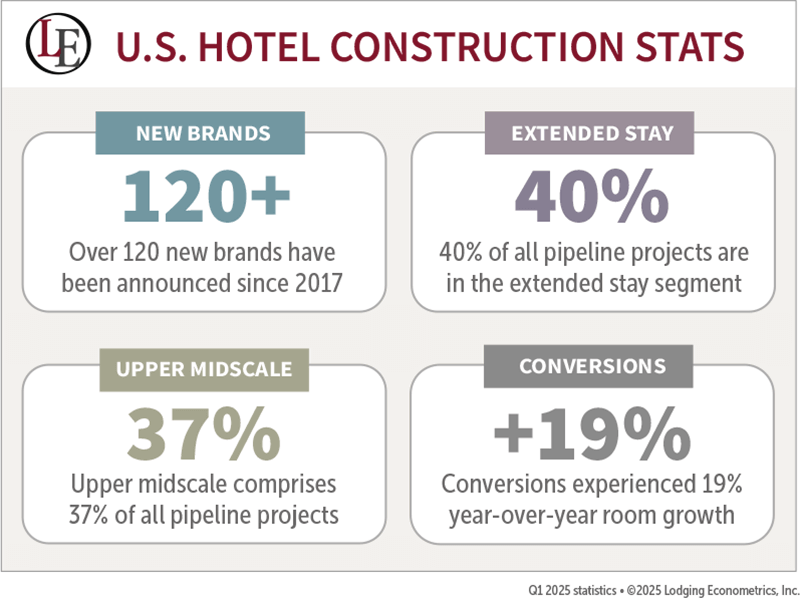

The expansion of the U.S. hotel construction pipeline is being driven in large part by the introduction of more than 120 new brands since 2017 and focused development in two high-performing segments: the upper-midscale chain scale and extended-stay accommodations. Analysis of LE’s Q1 2025 data reveals the upper-midscale chain scale’s dominant position, commanding an impressive 37% of all pipeline projects and 30% of rooms—a clear indication that developers are targeting the sweet spot between affordability and premium amenities that appeal to both business and leisure travelers. Simultaneously, the extended-stay segment has emerged, over the years, as a powerhouse, representing 40% of pipeline projects (2,535 projects) and 35% of rooms (258,945 rooms), underscoring the shift in consumer preferences toward accommodations that blend hotel conveniences with home-like features. This robust growth in extended-stay properties reflects both pandemic-accelerated demand for longer-term flexible accommodations and developers’ continued recognition of the operational efficiencies for extended-stay facilities.

LE’s Q1 report also highlights another shift in hospitality development strategy, with brand conversions surging to record levels—1,421 projects (136,668 rooms), reflecting a 15% project and 19% room growth year-over-year. This acceleration toward conversions, forecast to nearly match new construction openings in 2025, indicates developers’ strategic pivot to asset repositioning and optimization amid elevated construction costs and tighter financing. The combined conversion and renovation activity reached an all-time high of 2,050 projects (269,435 rooms) at the Q1 2025 close, signaling that owners are increasingly focused on revitalizing existing properties to meet evolving consumer demands.

However, new project announcements entered the pipeline at a healthy pace in Q1, with 313 projects totaling 37,912 rooms, while construction starts remained robust at the end of Q1 totaling 181 projects accounting for 23,296 rooms. This suggests developers are moving forward despite economic uncertainties, demonstrating the cautiously optimistic development approach in early 2025.

The first quarter saw 161 new hotels (18,767 rooms) open across the U.S., with LE analysts projecting an additional 579 properties (64,781 rooms) to debut through year-end. This anticipated total of 740 new hotels (83,548 rooms) represents a 1.5% annual supply growth rate for 2025. The development momentum is expected to continue into 2026, with forecasts indicating 848 new hotel openings (92,892 rooms), further expanding room supply by 1.6% and reflecting sustained industry confidence in the long-term strength of the U.S. lodging market.

As the hospitality landscape continues to evolve, navigating these dynamic shifts requires actionable intelligence and strategic insight. The comprehensive data highlighted in this article represents merely the surface of Lodging Econometrics’ extensive analytics capabilities. Industry leaders seeking to capitalize on emerging opportunities need the competitive edge that comes from access to LE’s detailed developer, ownership and project team member portfolios, contact information, and project pipelines. For more information, contact Lodging Econometrics today at (603) 431-8740 ext. 0025 or [email protected].