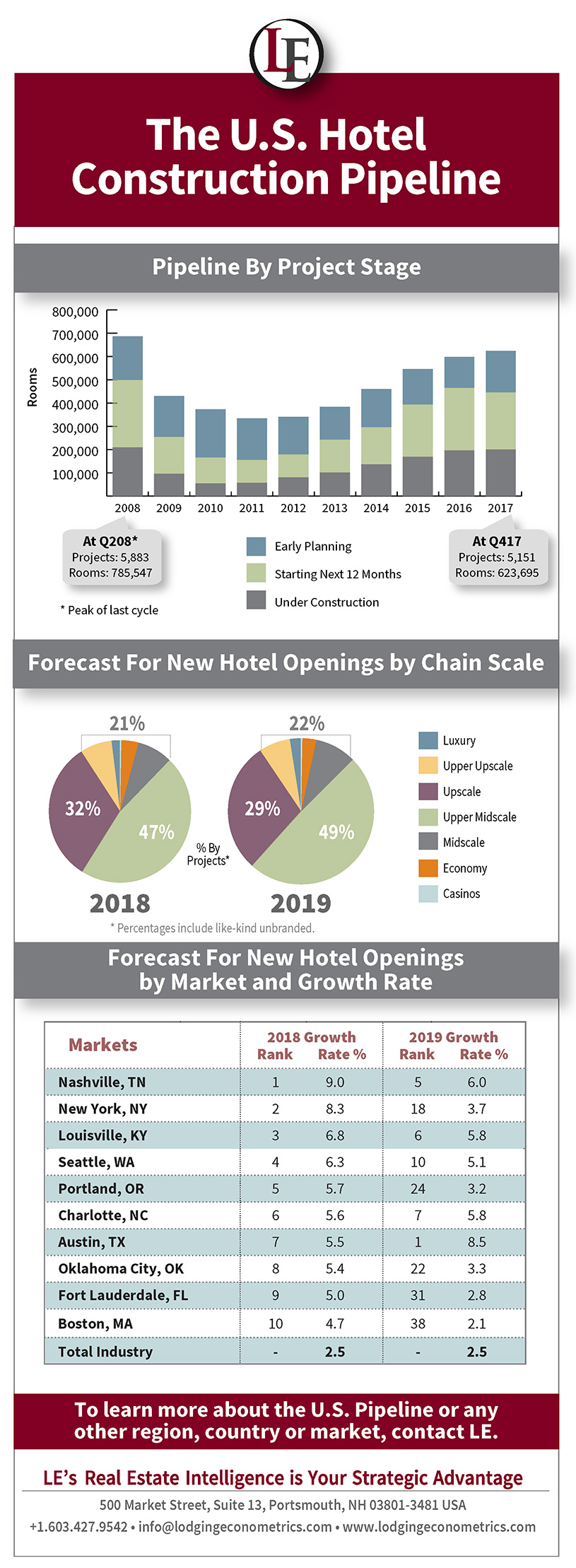

According to the year-end U.S. Construction Pipeline Trend Report from Lodging Econometrics (LE), the pipeline continued its upward growth trend in 2017 and stands at 5,151 projects/623,695 rooms, up 4% by projects and 4% by rooms year-over-year (YOY). There are 1,544 projects/200,632 rooms under construction, up 2% by projects and 2% by rooms YOY.

Projects in early planning are at 1,506 projects/177,849 rooms, up 44% by projects YOY. The rapid growth of new brands announced by major franchise parent companies in 2017 contributed to the increase in projects in the early planning stage. The end of the year also tends to encourage developers and brands to finalize franchise construction agreements and review timelines on existing agreements, both which contribute to an uptick in early planning.

2018 and 2019 Forecast for New Hotel Openings

By the end of 2017, 975 hotels/116,838 rooms had opened in the U.S., accounting for a supply growth rate of 2.3%. According to analysts at LE, the total 2018 forecast for new hotel openings is 1,145 projects/130,209 rooms, representing a 17% increase in projects over 2017 and a supply growth rate of 2.5%.

Almost half of the hotels expected to open in 2018 are upper-midscale, at 535 projects/52,575 rooms, or 47% of the total pipeline. This is followed by upscale, at 364 projects/45,048 rooms. These two chain scales represent 79% of the 1,145 projects anticipated to open in 2018.

LE forecasts that supply will grow 2.5% in 2019 with the opening of 1,209 projects/137,546 rooms. Again, it is being led by the number of hotels expected to open in the upper-midscale and upscale segment.

The top markets forecasted to grow their guestroom supply in 2018 are: Nashville, TN; New York; Louisville, KY; Seattle; Portland, OR; Charlotte, NC; Austin, TX; Oklahoma City; Fort Lauderdale, FL; and Boston.

In 2019, most of these markets with the exception of Austin, TX, which will become the market with the highest rate of growth for new hotel openings in the U.S., and Charlotte, NC, will all see a decelerated rate of growth. These other markets, however, will still be on par with or remain higher than the national growth rate of 2.5%.

For more information on the state of the construction pipeline or the forecast for what’s ahead in the United States or any other region, country or market worldwide, please contact Lodging Econometrics at (603) 427-9542 or email: [email protected].

JP Ford, SVP, director of business development, Lodging Econometrics

Bruce Ford, SVP, director of global business development, Lodging Econometrics

Tom O’Gorman, VP of sales, Lodging Econometrics