Since late 2024, hotel demand and average rates started to level off after a period of rapid growth throughout the COVID recovery. Market disruption in 2025 that started midway through Q1 related to the tariffs and government budget cuts caused softening hotel demand. As we enter 2026, in spite of continued uncertainty related to tariffs, the Middle East war and inflation and interest rate concerns, there seems to be resilience at the upper tier but some muting of hotel demand, particularly in the middle and lower tiers.

Occupancy and ADR Trends June 2025-March 2026

(4-week moving average)

In spite of market turbulence, Q1 2026 hotel performance appears to be generally moving to positive territory. This chart compares YoY ADR and Room Night demand with a moving 4-week average from June 2025 through March 28, 2026 and illustrates encouraging trends. The average rate (ADR) gained strength in Q4 2025, which persisted in 2026, especially in comparison to a difficult February and March in 2025. Demand has remained closer to previous year levels throughout this time period but had a good start to the year in 2026, before softening through March. Recent demand softness may be a short-term reaction to the Middle East war and related energy disruption.

Demand by Segment

(YoY Q1 2026—thru Mar 28)

While showing a 2% gain in overall year-over-year demand, we observe a similar pattern as the last two years where growth is coming from discount rate categories such as Promotion/Loyalty Member Rates and OTA. Corporate and Group demand remains slightly below last year at -1% while Rack/BAR volume appears to have shifted into the other rate categories showing a decline of -6% over 2025.

Location Types

(YoY Q1 2026—thru Mar 28)

All but rural/interstate locations are positive compared to Q1 2025. Corporate business is mixed showing growth in small city/towns and resort destinations with other locations down 1-3%. Government business is down compared to 2025 across all location types, but that is a reflection of the staffing and program cuts that didn’t begin until the latter part of Q1 2025. It is likely the government YoY comparisons will improve throughout 2026.

Performance by Market Q1 2026 vs. Q1 2025

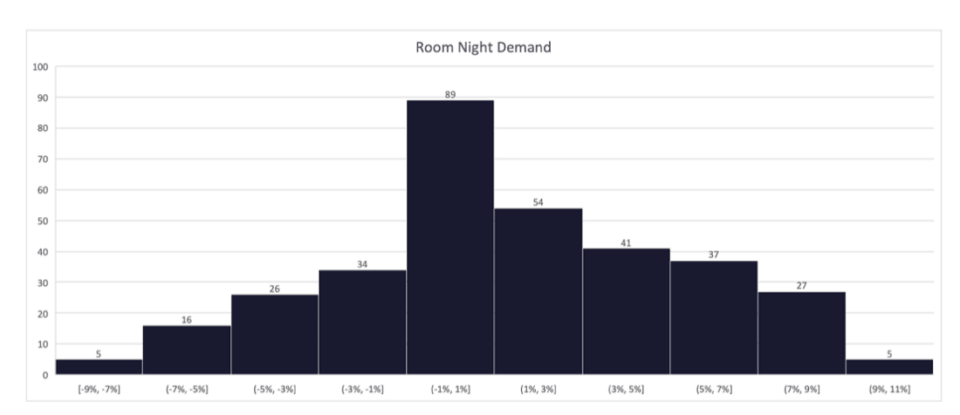

When looking at the 334 markets tracked by Kalibri, the performance leans in a positive direction for room night demand and even more so for ADR growth.

- Room nights: there are 89 (27%) markets flat to last year with 81 (24%) down by -1% to -9% compared to 2025 and 164 (49%) markets that are +1% to +11% better than 2025. Similar results are reflected in the 975 submarkets tracked by Kalibri.

- For ADR, there are 66 markets (20%) flat to last year. There are 199 markets (60%) that are +1% to +10% growth in ADR and 69 (21%) that are down compared to 2025 by -1% to -9%.

Room Night Demand 2026 vs. 2025 by Market

ADR 2026 vs. 2025 by Market

Summary

With uncertainty in the market, economically and geopolitically, it’s difficult to see a straight line in the data to anticipate how the year’s performance will play out. Lower and middle-tier hotels in secondary and tertiary markets are challenged more by demand and rate growth, but expense growth has not abated across all sectors of the hotel industry. Profit First techniques are increasingly important to all when economics face turbulent times. Expenses continue to rise with inflation and in response to energy and supply chain disruption leading hotels to take more definitive steps to automate and change processes to enable more efficient revenue acquisition and operational results.