NATIONAL REPORT—In order to provide some perspective to the current operating environment, CBRE Hotels Research took a look at the performance of the U.S. lodging industry during the previous 11 economic recessions.

CBRE’s Original 2020 Forecasts

The U.S. lodging industry was prepared for a slowdown in performance entering 2020. CBRE Hotels Research was projecting a 1.1% increase in RevPAR for the year. Even with this low level of revenue growth, there were certain factors that could have sustained—or at least cushioned the blow of minimal declines—the nine-year trend of profit growth for U.S. hotels since 2010.

- We are in a low inflation period, which keeps the cost of goods and services low.

- Recent changes to food and beverage operations and marketing practices have helped to lower fixed costs.

- There is no energy crisis, so utility costs remain low.

- Profit margins are 450 basis points (bps) greater than the long-run average.

- Constant dollar profits are 21.8% above the long-run average.

Obviously, the operating landscape has changed with the impact of the COVID-19 virus. CBRE Hotels Research is continually monitoring the latest lodging performance data and economic forecasts to prepare its projections of declines in occupancy, ADR, RevPAR and total revenue for 2020.

Impact on Profits

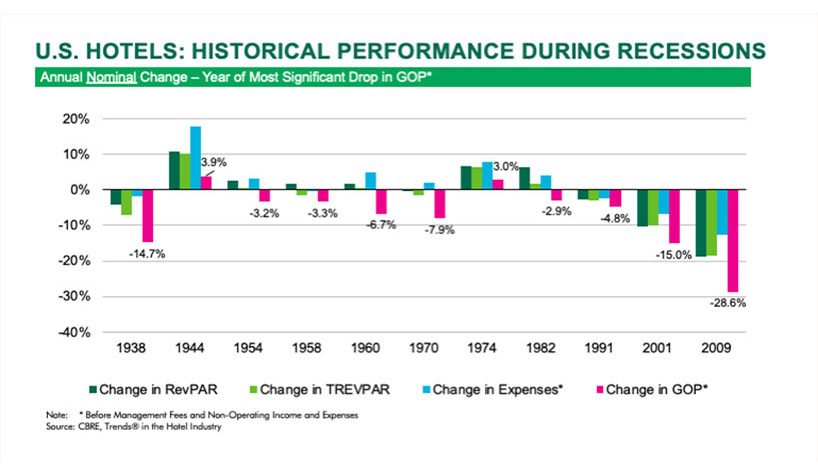

To provide some context to the expected declines in profits for U.S. hotels during 2020, CBRE analyzed the operating performance of properties during 11 economic recessions from 1938 through 2009. Lodging performance data comes from CBRE’s annual Trends in the Hotel Industry survey of operating statements dating back to 1937.

For each economic recession, CBRE analyzed hotel performance data for the year that the average hotel in its trends survey experienced the greatest decline, or least increase, in gross operating profits (GOP).

The average property suffered a nominal decline in GOP during nine of the 11 historical recessions. The two exceptions were the 1945 and 1973-75 recessions. The 1973-75 recession was characterized by high levels of inflation that masked the real decline in profits.

On average, over the 11 recessions, RevPAR declined by 0.9%, which resulted in a 2.3% decline in total operating revenue. Although hotel operators were able to limit expense growth to just 0.8% during the recession years, they still experienced a decline in profits. During the 11 historical recessions, the average property experienced a 7.2% decline in GOP.

Focus on 2001 and 2009

By far, U.S. hotels experienced the greatest declines in revenues and profits during the two most recent recessions; multiple properties experienced RevPAR declines in excess of 30%. It is assumed that the U.S. lodging industry will suffer a RevPAR decline in excess of 30% during 2020.

In 2001, of the trends survey properties that experienced a decline in RevPAR, only 2% saw RevPAR fall by more than 30%. On average, these properties suffered a 35.3% drop in total revenue, which resulted in a 54.2% decline in GOP.

During the 2009 recession, 10.2% of the properties that experienced a decline in RevPAR saw their rooms revenue drop by more than 30%. On average, these properties also suffered a 35.3% drop in total revenue, but the decline in GOP averaged 57.0%.

Comparing the two recessions, the 2001 RevPAR downturn was driven by a decline in occupancy, while the 2009 RevPAR decline was the result of almost equal declines in occupancy and ADR. Prior CBRE research has found that RevPAR declines influenced by ADR typically result in greater falloffs in profits. Further, the proliferation of intermediaries in the booking process between 2001 and 2009 increased the cost of revenue acquisition. Both of these factors contributed to the greater decline in GOP observed in 2009.

Given the low occupancy levels being reported by hotels around the U.S., most historical thumb rules will not apply during the spring and summer months. However, as currently anticipated, if we start to see signs of recovery toward the end of the year, some of these historical RevPAR/GOP relationships may be of value when assessing operating performance for the entire year.