1031 Exchanges are one of the most powerful tools in real estate, offering advantages for portfolio growth, diversification, estate planning and retirement. Yet many investors do not take advantage of this section in the tax code due to common misconceptions regarding the law, believing it is easier to “just pay the tax” without considering the benefits being left on the table. Likewise, the investor may believe that they are not eligible to do a 1031 exchange, being left with no option but to pay the tax. Below we will review the basics of a 1031 exchange, and then dive into specific advantages to hotel owners.

Basics and misconceptions of 1031s

1031 exchanges, at the most rudimentary level, defer taxes. Most understand that longterm capital gains taxes can be deferred, but equally important is the deferral of section 1250 depreciation recapture. Some taxpayers will do a linear move where they may not have a capital gain but wish to improve cash flow by resetting the depreciation timeline.

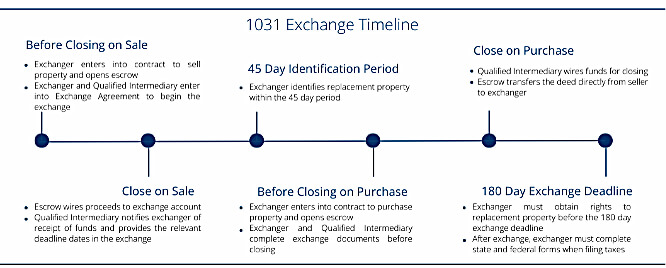

The rules of a 1031 tax deferred exchange are outlined in Section 1031 of the IRC. This is where we find the all-important exchange timeline, as shown above, but also where we have a common misinterpretation of the law. According to the Section 1031 of the IRC, no gain shall be recognized if exchanged for “real property of like kind.” Many wrongfully believe that “like kind” means the same asset class; however, all real estate is like kind with other real estate, as clarified in the Tax Cuts and Jobs Act of 2017. In fact, 1031 exchanges can be used to enter into Delaware Statutory Trusts (DSTs), and syndications (under the right conditions), which is helpful to remember if retiring or downsizing.

There are three general types of exchanges:

- Forward Exchange: The most typical. First sell (relinquish) a property, then use the sale proceeds to purchase replacement property, subject to timeline above.

- Reverse Exchange: Particularly helpful in tight markets, this is a situation where the replacement property is acquired prior to selling the relinquished property. The IRS has offered a safe harbor for reverse exchanges, as outlined in Rev. Proc. 2000-37, effective Sept. 15, 2000.

- Construction Exchange: This technique allows the taxpayer to build on, or make improvements to, the replacement property, using the exchange proceeds.

Benefits to hotel owners

Hotel owners have a unique opportunity to maximize the advantages provided by a 1031 exchange. As all hotel owners know, the value of a hotel is largely based on the business performance. Now what makes hotels unique? You are not able to “1031” a business, you are only permitted to “1031” real estate. However, hotels are both real estate and a business; they cannot be separated from each other like other asset classes. In the case of daycare centers, restaurants, body shops, etc., when sold with the real estate, the transaction is in two parts: the sale of the business and sale of the real estate, with only the real estate portion being exchangeable. This is not typically the case in hotel sales, where there is one transaction, meaning the entire value of a well-run operation can be brought into an exchange upon sale. Successful hotel owners have the ability to influence the sale price of their properties more than owners of other asset classes, while fully reaping the tax benefits of their value add.

Acquiring with debt

As eluded to earlier, it is common to hear “I just pay the tax, it’s easier,” but again, it is important to consider the next step. If the ultimate goal is to purchase another property with the sale proceeds by leveraging debt, even a small loss to a tax bill significantly lowers the amount a bank will offer in loans. Let’s consider a bank willing to fund 80% on a deal: at an 80/20 ratio, even a minor tax bill of $100,000 lowers the potential funding from the lender by $400,000. Now move the decimal—$1,000,000 lost to taxes could cost $4,000,000 in funding. In the graphic below, we can compare a conventional sale to a 1031 exchange sale.

Final thoughts

While the general concept of a 1031 exchange may be quite simple, it can easily be complicated with issues such as partnership dissolutions, carry back financing and more. It is best to find a qualified intermediary that is willing to take the time to listen to your unique situation, accurately analyze the facts and law, and offer proper guidance. There are significant implications whether choosing to exchange or not, and it is important to obtain sound, informative advice on your options. Lastly, the 1031 exchange industry remains largely unregulated. Seek a qualified intermediary that provides security of funds, legal competence and real estate expertise.

Andrew Favorito is VP/senior exchange officer at City Capital 1031, which serves as a qualified intermediary nationwide. Specializing in hospitality transactions, he brings industry specific experience from over a decade in hotel management.

This is a contributed piece to Hotel Business, authored by an industry professional. The thoughts expressed are the perspective of the bylined individual.