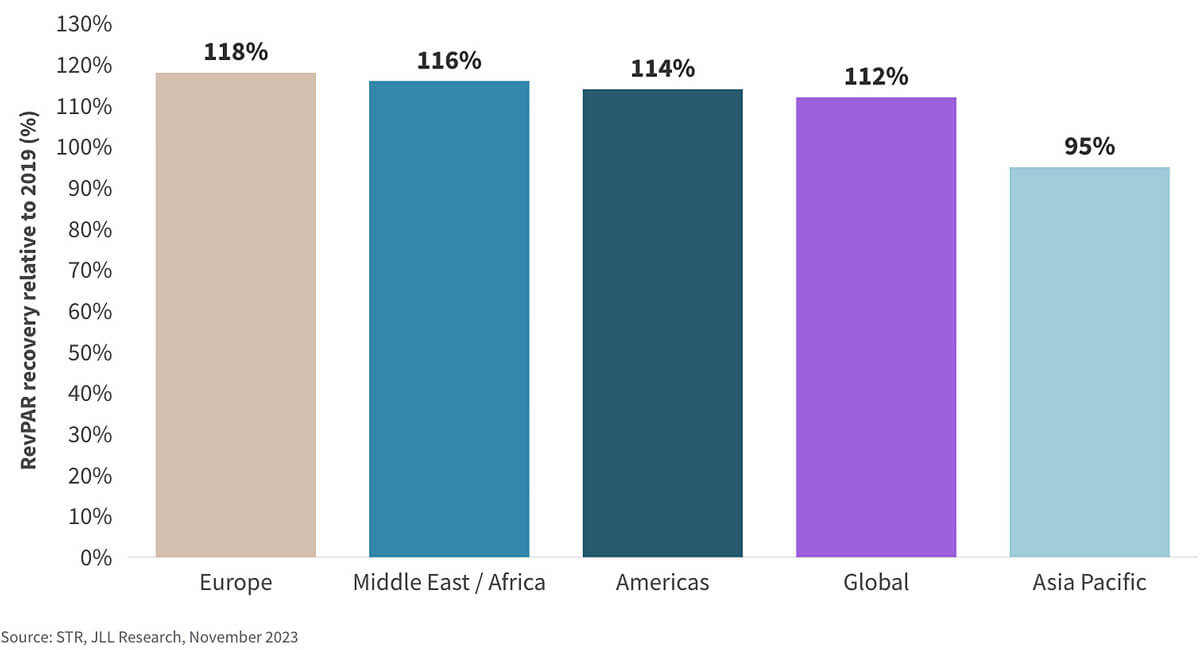

While global hotel RevPAR remains elevated, surpassing 2019 levels by 11.7% through the first 11 months of 2023, performance has begun to normalize as some leisure travel contracts. Stabilization has weighed heaviest in resort markets, predominantly in the Americas and EMEA, with Asia-Pacific continuing to accelerate as intraregional travel grows following border reopenings, according to JLL’s Global Real Estate Perspective February 2024. Global urban market performance is strengthening, propelled by a surge in international travel and the return of business and group demand. Markets like London, New York and Tokyo are expected to lead global RevPAR performance in 2024 as travelers continue to return to cities.

Future trends: Surging international travel to drive urban hotel performance and fuel liquidity

Outlook for 2024: Following the removal of all post-pandemic restrictions, global international travel surged in 2023, reaching 87% of 2019 levels. The effect on urban hotel demand cannot be understated as historically there has been a 90% correlation between inbound foreign arrivals and urban hotel occupancy, with the greatest impact in gateway markets such as London, New York and Tokyo. We expect international travel to accelerate further, with Europe likely the largest beneficiary as it prepares for the Summer Olympics in Paris and Taylor Swift takes her Eras Tour to the U.K. and Western Europe. This pickup in travel should also fuel global hotel liquidity. Foreign capital, which has been largely absent since the onset of COVID, is anticipated to be increasingly active over the next 12 months. Middle Eastern and Asian investors will likely be the most acquisitive, with urban markets in Europe and select U.S. cities the largest beneficiaries of capital.

Long-term: With 1,350 global hotel brands to choose from, investors must be increasingly discerning in the brand they choose to acquire; they are now buying into an entire ecosystem as traditional hotel brands expand into adjacent verticals with the goal of capturing the entire travel journey and solidifying an indelible sense of loyalty. Branded residences, private membership clubs and even yachts have become more and more integrated into traditional hotel brands’ portfolios, creating new opportunities for investment. As global hotel development slows amid rising construction costs, brand platform acquisitions are expected to drive shareholder value and become a major focus for investors over the long term. Brands in the luxury and lifestyle space are likely to garner the most investor interest, such as PIF’s recent $1.2 billion investment into Rocco Forte hotels.