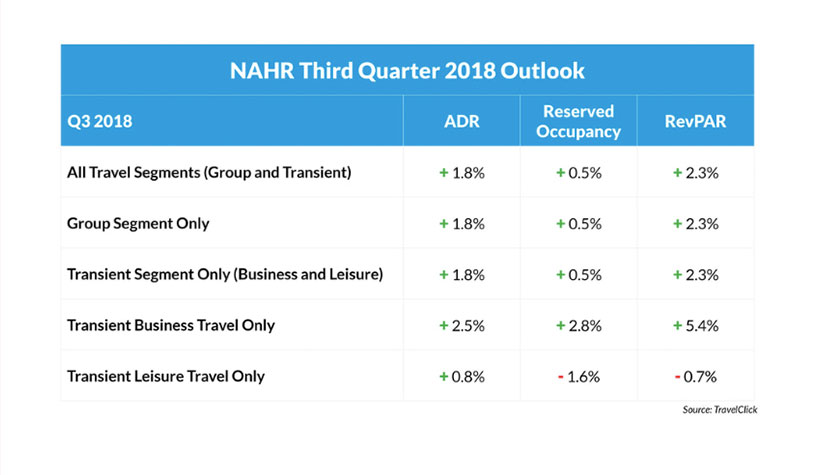

NEW YORK—The second half of the year has stable rates and bookings across all travel segments, up 1.8% in ADR and 0.51% in bookings in the third quarter when compared to the prior year, according to new data from TravelClick’s August 2018 North American Hospitality Review (NAHR). Group travel in Q3 is also up 1.81% in ADR and 0.5% in bookings, and the transient segment overall is up 1.8% in ADR and 0.52% in bookings in the same time period.

Transient business travel, however, is experiencing more pronounced growth for the quarter, up 2.56% in ADR, 2.81% in bookings and 5.45% in RevPAR.

“The outlook for the remainder of Q3 and Q4 RevPAR growth is continuing on the positive trajectory that occurred in the first half of 2018,” said John Hach, senior industry analyst for TravelClick. “While new reservation pace is gradually slowing, there is still organic growth in the majority of North American markets. This growth, coupled with steady ADR increases, is sustaining a profitable marketplace for most North American hoteliers.”

Twelve-Month Outlook (August 2018 – July 2019)

For the next 12 months (August 2018 – July 2019), transient bookings are up 0.5% year-over-year, and ADR for this segment is also up 2.7%. When broken down further, the transient leisure (discount, qualified and wholesale) segment is down -1.7% in bookings, but ADR is up 2.1%. In addition, the transient business (negotiated and retail) segment is up 3.6% in bookings and 3% in ADR. Lastly, group bookings are up 0.7% in committed room nights over the same time last year and ADR is up 1.9%.

“Despite the current growth of the industry, there are indications that 2019 reservation growth will be less consistent than 2018,” added Hach. “TravelClick’s forward-looking business intelligence data is currently showing a reduction in next year’s advance group reservation pace. Thus, it is incumbent that hoteliers who are heading into their 2019 budgetary planning sessions take into consideration the changing marketplace, especially when it comes to allocating adequate marketing funds to compete for transient demand throughout next year.”

|

Q3 2018 |

ADR |

Reserved Occupancy |

RevPAR |

| All Travel Segments (Group and Transient) |

1.80% |

0.51% |

2.33% |

| Group Segment Only |

1.81% |

0.50% |

2.32% |

| Transient Segment Only (Business and Leisure) |

1.80% |

0.52% |

2.33% |

| Transient Business Travel Only |

2.56% |

2.81% |

5.45% |

| Transient Leisure Travel Only |

0.88% |

-1.63% |

-0.76% |

|

Source: TravelClick |

|||

|

Q4 2018 |

ADR |

Committed Occupancy |

|

| All Travel Segments (Group and Transient) |

2.0% |

1.3% |

|

| Group Segment Only |

1.0% |

2.3% |

|

| Transient Segment Only (Business and Leisure) |

2.4% |

0.1% |

|

| Transient Business Travel Only |

1.8% |

3.0% |

|

| Transient Leisure Travel Only |

2.0% |

-1.8% |

|

|

Source: TravelClick |

|||

The August NAHR looks at group sales commitments and individual reservations in the 25 major North American markets for hotel stays that are booked by Aug. 1, 2018, for the period of August 2018-July 2019.